Getting The Fast Approval Payday Loans To Work

What Does Fast Approved Cash Loans Do?

However the lender usually won't stop with one effort. It keeps attempting to gather the cash, frequently breaking up the payment into smaller sized amounts that are most likely to go through. And, at the very same time, the lender starts harassing you with calls and letters from attorneys. If none of that works, the lender will probably sell your debt to a collections firm for cents on the dollar.

If it wins, the court can allow the company to seize your possessions or garnish your salaries. Payday lenders generally don't check your credit prior to releasing you a loan. For such small loans at such short terms, it's just too costly to run a credit examine every one. However, if you stop working to repay your loan, the credit bureaus can still learn about it.

All About Instant Loans With Bad Credit Ok

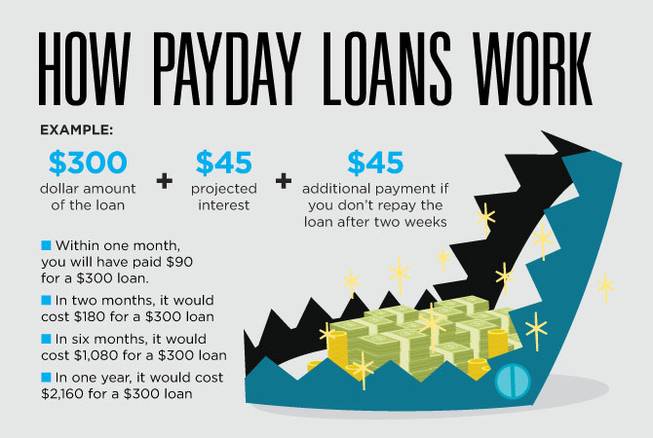

Yet if you do repay the loan on time, that payment most likely will not be reported to the credit bureaus, Find more info so your credit report won't improve. The biggest problem with payday loans is that you can't pay them off slowly, like a home mortgage or an auto loan. You have to come up with the entire amount, interest and principal, in just two weeks.

According to the Consumer Finance Security Bureau, roughly 4 out of five payday loans end up being renewed or rolled over to a brand-new loan. The laws about payday financing differ from one state to another. States fall under 3 standard groups:. In 28 states, there are extremely couple of limitations on payday financing.

The Of Bad Credit Loans Approved By Lenders

However, even these states have some limitations. Many of them put a limitation on just how much money users can obtain either a dollar amount or a percentage of the debtor's regular monthly income. Likewise, a federal law bars lenders in all states from charging more than a 36% yearly percentage rate (APR) to active-duty members of the military.

In 15 states, plus Washington, D.C., there are no payday loan workplaces at all. Some of these states have actually prohibited payday loaning outright. Others have actually put a cap on interest rates typically around 36% APR that makes payday financing unprofitable, so all the payday loan offices have closed. Nevertheless, customers in these states can still get loans from online payday lenders.

The Bad Credit Fast Payday Loans PDFs

Some cap the interest payday lenders can charge at a lower rate typically around $10 for each $100 borrowed. This exercises to more than 260% yearly interest based upon a two-week term, which is enough for payday lenders to make an earnings. Others restrict the number of loans each debtor can make in a year.

Not known Facts About Direct Payday Lenders Approved Loans

Not known Facts About Direct Payday Lenders Approved Loans

For example, Colorado passed a law in 2010 requiring all loans to have a regard to at least six months. As an outcome, most payday lenders in the state now permit borrowers to pay back loans in installations, rather than as a lump sum. The Bench report shows that in states with more stringent laws, fewer people take out payday loans.

The Facts About Bad Credit Loans Approved By Lenders Revealed

The 30-Second Trick For Bad Credit Fast Payday Loans Guaranteed

The 30-Second Trick For Bad Credit Fast Payday Loans Guaranteed

People in limiting states still have access to online lenders, but they disappear likely to use them than people in permissive states. In June 2016, the Customer Financing Security Bureau proposed a brand-new rule to regulate payday lending at the national level. This guideline would require lenders to examine customers' earnings, expenditures, and other financial obligations to make sure they can pay for to repay the loan.

And lastly, it would require lenders to let borrowers know prior to pulling cash out of their checking account and restrict the variety of times they can attempt to withdraw money before quiting. This guideline hasn't taken impact yet, and lots of payday lenders are hoping it never ever will. The CFSA launched a statement claiming this rule would force payday lenders out of organisation.

The Single Strategy To Use For Bad Credit Fast Payday Loans

The issue is, the proposed rule does not do that. Rather, Bench states, it would let payday lenders keep charging triple-digit rate of interest while making it harder for banks to offer much better, cheaper options. Bench has actually proposed its own guideline that would restrict short-term loans, but would encourage longer-term loans that are simpler to pay back.

However, this so-called alternative which is unlawful in about half the states in the nation is actually just a payday advance loan in disguise. When you take out an automobile title loan, the lender analyzes your car and offers you a loan based on its worth. Typically, you can get up to 40% of the vehicle's value in money, with $1,000 being the average amount.

Some Of Bad Credit Fast Payday Loans Guaranteed

https://www.youtube.com/embed/Mx6Ve4iID1Y

Vehicle title loans have the exact same short terms and high interest as payday loans. Some are due in a swelling sum after one month, while others get paid in installations over 3 to 6 months. Together with interest of 259% or more, these loans also consist of fees of as much as 25%, which are due with your last payment.